Deep Dive: Mercado Pago & Digital Banking in Latin America

Mercado Libre has an answer for Latin Americans seeking modern banking solutions.

Twenty years ago, history was made.

Mercado Libre (MELI), the Argentinean retailer which had itself been launched just four years earlier in the dot-com heyday of 1999, was riding high following successful entries into major markets such as Brazil and Mexico. The company’s leadership rolled out a new secure system to diversify payment options on its online marketplace and serve as a trusted escrow between buyers and sellers.

This new payment system was called Mercado Pago, and it’s a prime success story for the fintech (“financial technology”) craze taking Latin America by storm. In fact, despite predating the worldwide explosion of fintech interest by more than a decade, it’s quite clear the company, which handles all financial services for the greater MELI ecosystem, is here to stay.

Mercado Pago’s leadership clearly predicted the fintech boom that has made Latin America one of the most dynamic regions in the world for banking services. But how has it done in the twenty years since its founding?

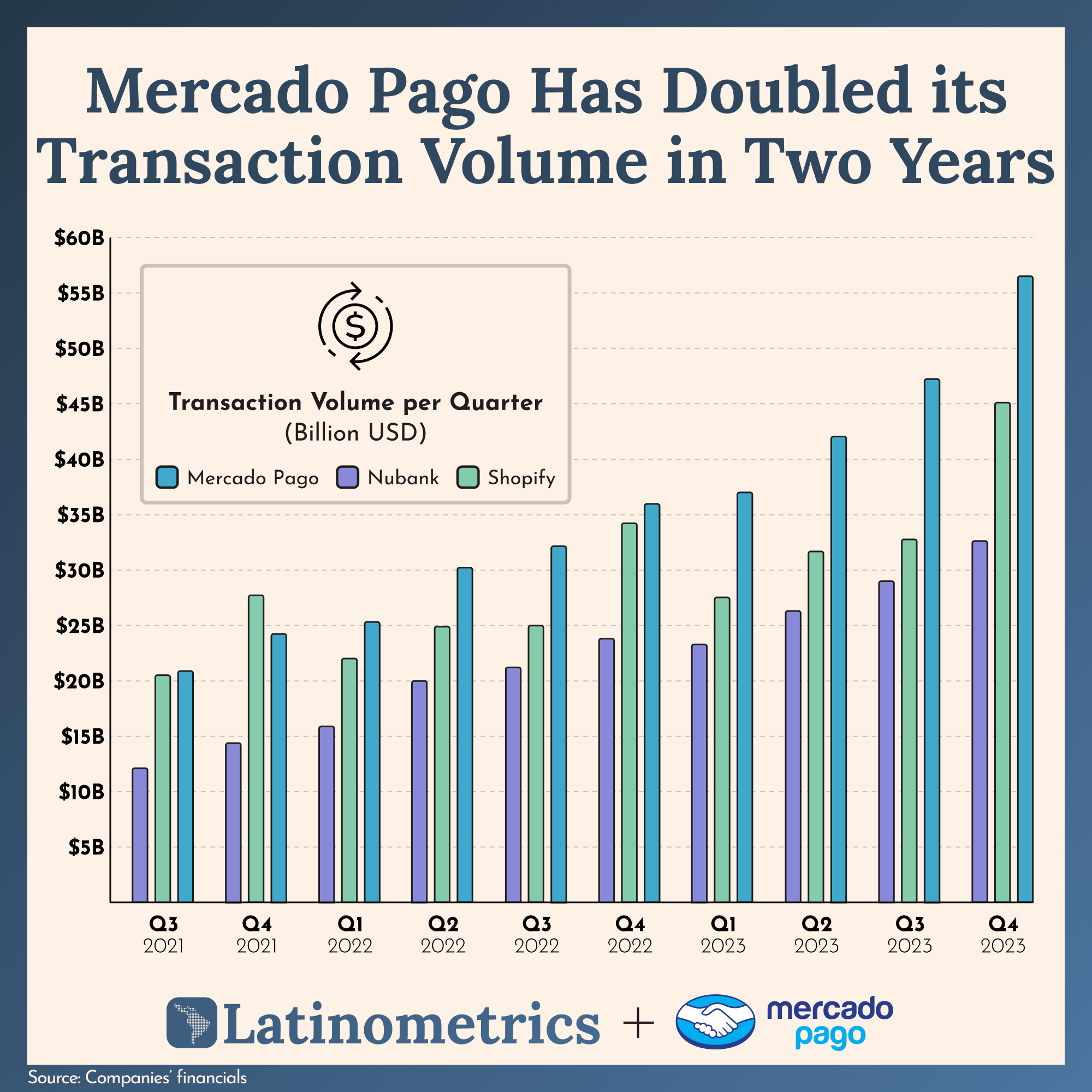

Well, you tell us. The company reached 53M active fintech users in the final quarter of last year—over the total population of its birthplace, Argentina. What about transactions? Mercado Pago’s transaction volume has doubled since just 2021, reaching over $55B at the end of 2023.

In the below chart, we take a look at some of the numbers involved, holding up the quarterly transaction volume handled by Mercado Pago in comparison with Nubank (which operates across Brazil, Mexico, and Colombia) and Shopify (a Canadian retail giant operating across multiple continents). Breaking down some of the figures made publicly available by each of the companies, it’s clear that – whether in or out of the MELI marketplace – Mercado Pago is on top with the over $55B it reported last quarter.

Clearly, Mercado Pago has exploded in popularity in recent years. The MELI subsidiary has rolled out feature after feature to become a one-stop shop for Latin American citizens seeking to access financial services, reflecting a clear understanding of the market today and where the region stands in terms of banking needs.

Today, Latin America presents a mixed picture when it comes to the banking industry. An overwhelming majority of Brazilians, for example, possess a financial account and/or debit or credit card. Brazil is the banking capital of the region, hosting all five of the region’s largest banks, while also seeing strong government policy in recent years to facilitate the ease of use for most account holders through successful instant payment systems such as Pix.

For many Latin Americans, however, the reality is different. Less than half of all Mexicans are banking today, with lower-income sectors of the country in particular still relying on cash for daily transactions and business expenses. This is doubly the case in rural areas in the country’s interior, as well as states in the far south such as Chiapas.

Most other countries in the region fall between those two realities, though it’s Chile which leads its peers with roughly 80% of Chileans accessing financial institutions, no doubt thanks in part to decades of macroeconomic stability. Central Americans of all stripes are on the lower end of the spectrum, with Costa Rica emerging as a notable exception. Meanwhile, less than a third of Paraguayans have a bank account; less than a fifth even possess a payment card.

With range like this, it’s evident that there’s nothing if not opportunity in the region for nontraditional players to make a big splash in the banking industry. Being able to overcome the usual barriers for people to access financial institutions, such as cost or accessibility, is essential for moving the industry forward. Even more key is taking advantage of the evolving digital world—Latin America’s smartphone adoption rate reached 79% in 2022. This is particularly the case in major markets such as Brazil, Argentina, and Mexico.

Enter those fintechs we mentioned earlier, which include innovative companies we’ve covered before such as Nubank and Mexico’s Spin. None have the reach and overall region-wide presence of Mercado Pago, which currently operates in 8 Latin American countries.

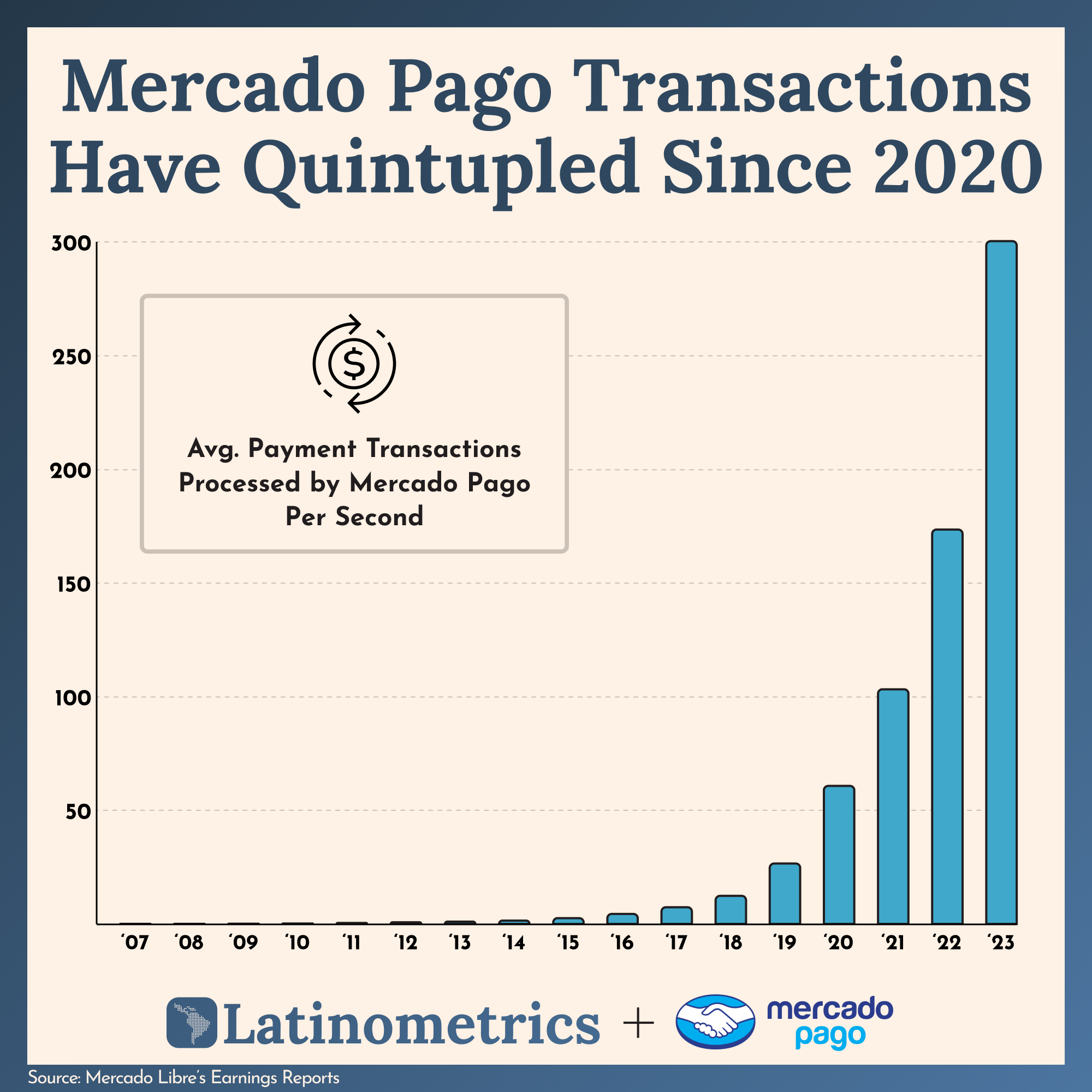

Today, go anywhere from the Copacabana boardwalk to the tianguis of Mexico City and you can bet you’ll find the company’s classic bright blue payment processor. In fact, the number of average payment transactions handled by the company has grown by more than 5x since 2020. It now processes, on average, 300 transactions per second.

This strong position is hard-earned, coming after 20 years of fine-tuning the service to match consumer needs across each of its core markets. In pursuit of financial inclusion that promotes payment services to traditionally underbanked populations, Mercado Pago has long since superseded a mere digital wallet that can pay bills, transfer money, and make online payments.

Today, users across Latin America can access insurance, prepaid and debit cards, and even lending services. Meanwhile, vendors and merchants can utilize Mercado Pago point-of-sale devices to allow for mobile card payments across their businesses.

At the core of all this is a single application, designed to turn anyone’s smartphone or computer into the center of their banking and financial needs.

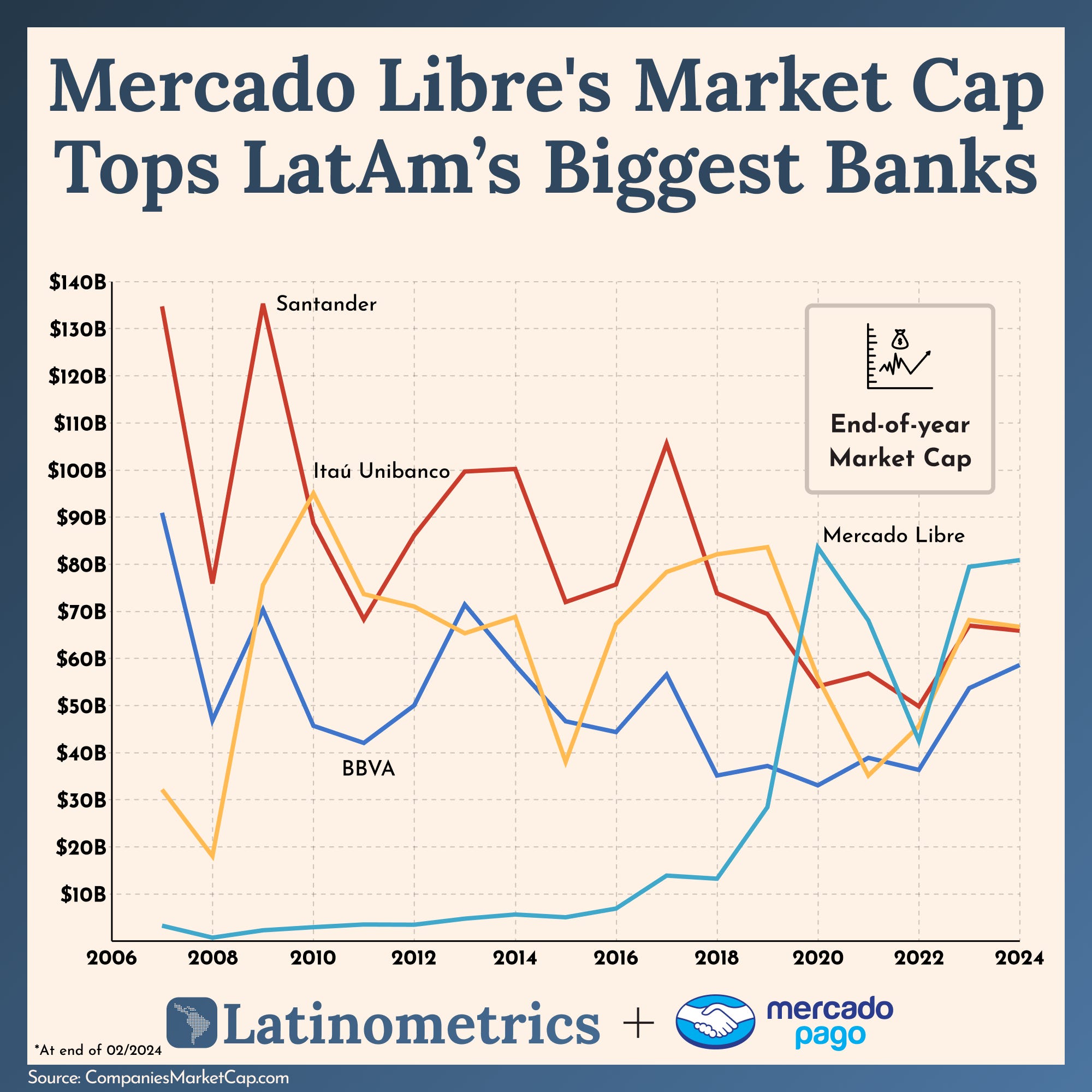

If all this sounds like a recipe for success, it’s because it absolutely is. Powered primarily by growth in Mercado Pago as a financial solution for Latin Americans everywhere, the MELI parent company has soared to new heights. Today it counts a market capitalization of close to $80B, well ahead of even established, regionally hegemonic banks like Itaú Unibanco, BBVA, and Santander.

So the next time you hear somebody call Mercado Libre just “Latin American eBay,” it’s worth reminding them that today the company is in a whole different league. On the back of Mercado Pago’s widespread adoption as a leading financial services provider in the region, the MELI ecosystem has become an essential part of Latin America’s banking scene. And at its core is a service more akin to a mixture of PayPal, Square, and Revolut.

Today more people are being connected to their money, with more money thus being transferred and moved around, meaning greater connectivity and growth for the region as a whole. To top it all off? The application is even integrated with major national payment services like Brazil’s Pix system, meaning people lacking access to traditional banks have never had an easier time taking control of their money.

We’d like to finish with a small consideration of time. As we’ve shown, in the last 20 years Mercado Pago has grown to be an inextricable part of Latin America’s financial industry. It’s successfully cast off early peers like N26 or Spin to instead become a giant competing with 19th-century banks like Santander or BBVA.

So what will the next 20 years bring? Will the company expand from its current offerings to the rest of the region—or indeed, even outside of Latin America? Will it grow its presence within the insurance or even mortgage sectors?

We’re not sure of the answers, but we bet that Mercado Pago’s growth will mean more financial inclusion for everyday Latin Americans. And you can bet we’ll be following along closely.